“True leadership isn’t about being in charge,

it’s about taking care of those in your charge.”

DAVID MELTZER

The Podcast

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

Welcome to our June newsletter

The end of the financial year is hurtling towards us. Much has happened since my last newsletter — not least, the federal election. Labor scored a landslide victory, while the Liberals were nearly wiped out.

But it does raise questions about the voting system. Despite the result, Labor secured just 34.6% of the national primary vote. The Liberal–National Coalition managed 31.6%. That means two-thirds of voters didn’t give their first preference to either major party. The combined primary vote for Labor and the Coalition fell to 66.2% — the lowest since the 1930s.

It’s a clear sign Australians are turning away from the major parties — and looking for alternatives. That makes policymaking harder to predict and potentially more volatile.

Expect Labor to push ahead with its controversial tax on unrealised capital gains inside super — and to double down on policies like the shared equity housing scheme. But with the Greens and independents now holding even more sway, the pressure will be on for new taxes on wealth and further intervention in the housing market.

We’re in uncharted waters. Stay informed — and stay strategic. And remember: if you take care of the things in your life you can control, you won’t need to lose sleep over the things you can’t.

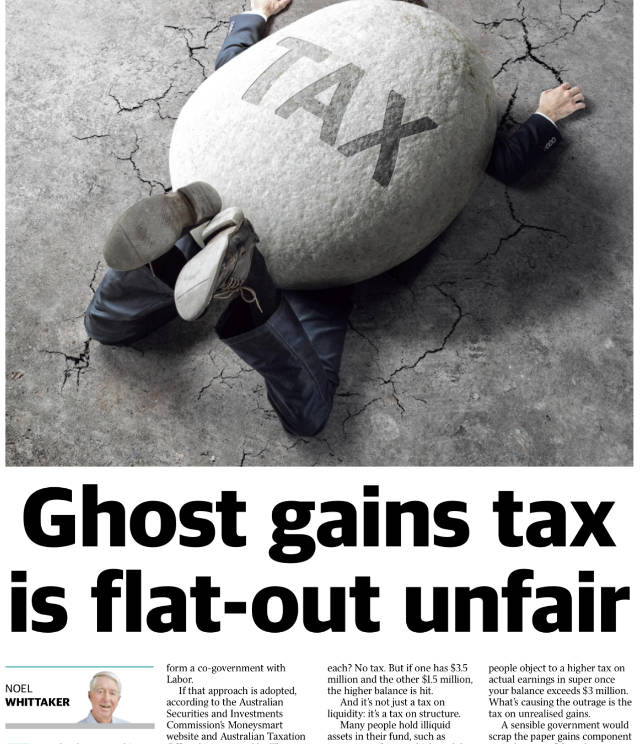

Taxing unrealised capital gains

Labor’s proposed tax on unrealised capital gains in super is finally getting the attention it deserves, as more Australians grasp just how draconian the policy really is. It’s a textbook example of unintended consequences – a slick-sounding policy with the potential to wreak financial havoc. It must have been an irresistible proposition: let’s put a special tax on the rich; there’s not many of them, and they don’t vote for us anyway.

Welcome to Australia’s Animal Farm, where all super funds are equal, but some are more equal than others. Judges and public servants retiring on massive defined benefit pensions, often worth well over $3 million, have been handed a special exemption. Why? Because taxing them was deemed “too hard” – while everyone else above the cap is expected to pay up. The hypocrisy is breathtaking.

The proposed tax is also a form of double taxation. Under this plan you’ll pay an extra 15% tax each year on the nominal increase in value of your super assets — even if you haven’t sold anything. When you do sell those assets and realise a profit, you’ll pay capital gains tax. And no, there’s no credit for tax already paid on the unrealised gains.

Labor have never made any secret about their hatred of self-managed super funds. Every dollar in an SMSF is one less dollar paying fees to the Labor-dominated industry super funds. But SMSFs let people hold assets not open to the big funds – business premises, farms, and commercial property – none of which can be sold at the click of a button. If taxes on paper profits force enough people to liquidate at once, prices will collapse; it’s simple supply and demand.

And make no mistake – Australians will respond. Many I’ve spoken to are already planning to restructure by gifting to children: helping them buy property, pay down loans, or invest. That shift – combined with likely interest rate cuts later this year – could fuel another property boom. It’s the opposite of what the government claims it’s trying to achieve.

If this tax becomes law, it will also impede innovation. Many tech founders launch start-ups through their super funds, and these businesses are often illiquid for years. Their perceived value can fluctuate wildly. Imagine a $1 million start-up growing to $6 million on paper — triggering a tax on a $5 million gain that may never be realised. If the valuation crashes to $3 million the next year, the fund is still taxed on money that never existed. Madness.

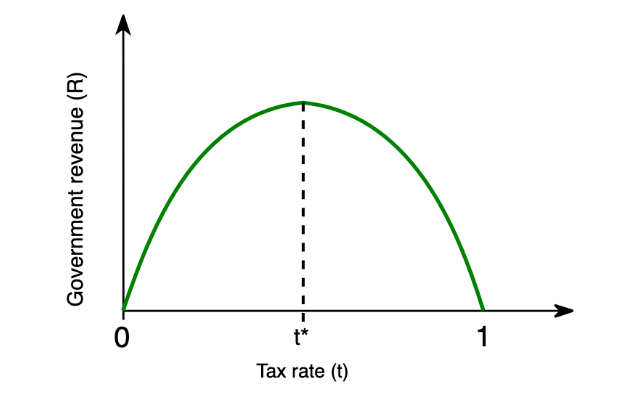

And let’s not forget the Laffer Curve: the well-established principle that raising tax rates beyond a certain point actually reduces total tax revenue.

Push people hard enough, and they’ll restructure, withdraw, or move their wealth offshore. So a tax designed to raise more money might end up collecting less.

But the biggest danger is this: it’s a foot in the door for taxing wealth that doesn’t exist. Once you accept that principle, no asset is safe.

If it’s okay to tax unrealised gains for someone with $3 million in super – or $2 million if the Greens get their way – what stops a future government from applying the same logic to investment properties? Or a share portfolio? Or a business? And then there’s the family home. Right now, your principal residence is tax-free, even if it’s worth $100 million. But it stands out like a beacon for any government desperate for cash and bold enough to grab it.

Once that line is crossed, there’s no telling where it ends. You may think this policy doesn’t affect you, but to quote John Donne: “Never send to know for whom the bell tolls; it tolls for thee.”

What to do now

For most people, the key message is: don’t panic and sell assets willy-nilly. Provided your super balance is under $3 million per member on 30 June 2026, the new tax won’t apply to you.

A special case is those with large illiquid assets — such as farms or commercial buildings — held within an SMSF. In many cases, it may be worth obtaining a valuation as at 30 June 2025 at the highest justifiable value. This could reduce the size of any unrealised capital gain as at 30 June 2026.

But there’s always a paradox. A higher valuation now means a higher cost base, which could reduce your capital gains tax liability later if you sell. This is a complex area where expert advice is a must.

Remember, only a portion of the fund is subject to the new tax. For example, if your super fund is worth $4 million and there’s an unrealised capital gain of $300,000 in a given year, only 25% of that gain — or $75,000 — would be taxable. At the proposed rate of 15%, that equates to a tax bill of $11,250. That may be a better outcome than transferring assets out of super to another entity, which would likely trigger capital gains tax — and if real estate is involved, stamp duty as well.

It all comes back to careful modelling of every scenario — including the possibility of gifting assets to family members before 30 June next year.

Noel’s Next Presentation

I’m thrilled to advise that I’ll be visiting South Australia to get talks next month.

Topics will include:

- How much money you really need for a comfortable retirement

- Where to invest your money as you move through retirement

- How franked dividends work — and how to use them to your advantage

- Gifting strategies and how they affect Centrelink and estate planning

- What you need to know about wills, powers of attorney, and superannuation death benefits

This session is designed to be straightforward, free of jargon, and packed with tips you can use straight away. The presentation will run for around 45 minutes, followed by 15 minutes of open Q&A — so bring your questions!

Here are the links for booking and details of the venues and times:

Wednesday, 25 June – 6:30 pm – Mount Barker Community Library

Thursday, 26 June – 5:30 pm – Aberfoyle Park (Hub) Library

Friday, 27 June – 10:30 am – St Peter’s Library

I’d love to see you there!

Tax planning for 30 June

June 30 is rapidly approaching, which means it is time to seek advice about ways to save tax.

Image by rawpixel on Freepik

Image by rawpixel on Freepik

The end of the financial year is critical for capital gains tax purposes. Remember, CGT is not triggered until you dispose of the asset and you must have owned that asset for over 12 months to get the 50% discount. In this context, the appropriate date for CGT purposes is the date of the contract, not the date of settlement. If you’re thinking of selling a property talk to your accountant and decide whether it’s better to have the contract dated before June 30 or after June 30. If you choose after June 30, you have 12 more months to pay the CGT, but the most important thing is which tax bracket you’ll be in when you trigger it.

CGT is calculated by adding the capital gains to your taxable income in the year the sale has been triggered – often you can reduce the CGT by making tax deductible contributions to superannuation. A little known-strategy which can be great for retirees under 67, is to use catch-up contributions. The carry-forward rule lets you boost your concessional contributions (CCs) by using up any unused CC cap amounts from the previous five financial years. To be eligible, your total super balance must be under $500,000 just before the start of the financial year in which you want to contribute — and that includes all your super accounts combined. The rule kicked off in 2019–20, which means it’s now possible to make up to $162,500 in tax-deductible CCs this year if you haven’t used any of your caps since 1 July 2019. But don’t delay — any unused cap from 2019–20 will vanish after 30 June this year.

Making tax deductible superannuation contributions up to your maximum concessional cap of $30,000 a year is a no-brainer. Once you have reached that cap, consider making a contribution for your spouse. If they earn less than $37,000 this financial year you may even get a tax offset as a bonus. Get advice on your particular circumstances, as this tax offset is unlikely to be a better option than making a deductible contribution for yourself. To qualify for the spouse contribution tax offset of $540 all you need to do is make a $3000 non-concessional contribution, on their behalf. Your spouse may also like to consider making a non-deductible super contribution for themselves of $1,000, if they are eligible for a $500 government co-contribution.

A re-contribution strategy is worthwhile if you have access to superannuation, and are still eligible to make contributions. You could withdraw up to $360,000 tax-free, and re-contribute it as a non-concessional contribution, on which there would be no entry tax. By doing this you would convert a large chunk of the taxable component of your fund to non-taxable, and so alleviate substantial taxes for your inheritors if you died suddenly, and your superannuation went to a non-dependent.

The cap for concessional superannuation contributions is $30,000and for non-concessional superannuation contributions is $120,000 for the 2025 financial year. To make contributions to superannuation and to utilise these caps, your fund must receive your contributions by 30 June. If you have more than one fund, all contributions made to all of your funds are added together and counted towards contribution caps. You may also be eligible to carry forward any unused contribution caps to a later financial year (if your total superannuation balance is less than $500,000 on the previous 30 June).

Take advice if you are nearing age 75 because apart from the downsizing contribution, it may be your last chance to boost your superannuation. You could still use the bring-forward rule, which will allow you to contribute up to $360,000 as a non-concessional contribution, and so move funds to an area where tax will be zero once you start to draw a pension from your fund.

From the mailbox

Image by Freepik

Image by Freepik

“I first wrote to Noel many years ago when I was a young woman in my twenties. I had just finished reading Getting it Together on Christmas Day while at work, and I took the opportunity to write and thank him for writing it. To my surprise, Noel replied with a personal letter.

One quote from the book has stayed with me for decades:

“You will be the same in five years as you are today but for two things — the people you meet and the books you read.”

I believe it’s by Charlie “Tremendous” Jones, and it’s guided much of my personal and financial growth.

Now, as a more mature woman approaching 60, I want to say thank you once again. I’m happy to report that my retirement will be very comfortable, and I have no doubt that your advice played a big part in that. I’ve just finished the updated Super Made Simple and am halfway through Wills, Death & Taxes Made Simple. I think I might be turning into a finance nerd!

I have two young adult children (18 and 20), and unfortunately no longer have my original copy of Getting it Together. If you have a spare copy floating around, I’d love one to pass on to them. Kids always seem more open to wisdom from someone other than their parents!

Many thanks again, Noel.

Warm regards

Tracey”

I replied to Tracey explaining that Getting It Together has been replaced by The Beginner’s Guide to Wealth, as we felt the original title was too ambiguous. The new book carries the same core content, with some updated financial material added. It’s the right book for anyone starting out, as it captures the lessons and wisdom I’ve gathered through the ups and downs of my journey through life.

Health Matters

Dr. Eric Topol, a cardiologist and researcher, has studied “super agers”—people over 85 who remain healthy and active—to uncover what contributes to long life without chronic illness.

His findings, drawn from genetic research and lifestyle analysis, reveal that lifestyle choices matter more than genetics.

Dr. Topol outlines several key habits that support healthy aging:

- Exercise – Resistance and strength training are essential. Regular activity helps preserve muscle mass and mobility.

- Sleep – Prioritising quality sleep is vital. Using sleep trackers can help identify patterns and improve rest.

- Diet – A mostly plant-based diet, rich in fibre and low in sugar, supports longevity. Topol personally avoids processed foods and eats within an 8-hour window (intermittent fasting).

- Protein – He’s increased his protein intake, especially from sources like chicken and plant-based proteins, to maintain muscle mass.

- Technology – Topol embraces digital tools like sleep monitors, glucose trackers, and even gene sequencing to manage his health proactively.

- Supplements and Testing – He supports using supplements cautiously and believes personalised medicine—including DNA and microbiome testing—can provide valuable insights, though more studies are needed.

Topol, now 70, says he follows all the advice he gives. His overall message: it’s never too late to start making small, evidence-based changes that significantly improve health span—not just lifespan.

Beware scammers

It was a quiet Friday – until my inbox exploded. A distressed reader had just seen what she thought was a government announcement: from 1 June 2025, nobody would be allowed to touch their super until age 70. She was shocked and panicky. It was all news to me, so I asked her to send a screenshot.

What came back looked highly convincing. It was a professional-looking Apple News article featuring a photo of the Prime Minister, complete with quotes and policy details. It claimed the preservation age was being lifted to 70 and promised a “work bonus” to soften the blow.

I told her it screamed fake news, and I was right. But within hours, dozens more emails flooded in from readers who had seen the same article and were equally alarmed. That’s when I called the Tax Office. They confirmed what I suspected: it was total rubbish. We immediately issued a special bulletin to all my news subscribers to warn them it was a fake.

This is AI and social media being weaponised. A few clicks, and boom – scammers whip up a fake news release so real it fools half the country. They blast it out on email or Facebook, and their goal’s dead simple: get you to click. One wrong move, and your device is toast, your data’s swiped, or your identity’s gone. These scams aren’t just dodgy texts anymore: they’re polished, gut-punching lies built to spark fear and chaos.

And when it comes to superannuation – one of your most important assets – the stakes are high.

Let’s be absolutely clear: any major changes to superannuation rules, such as lifting the preservation age, would be front-page news. They’d be announced through formal channels, usually as part of the Federal Budget, and covered extensively in mainstream media. If you haven’t seen it on the evening news or read it in a major newspaper, chances are it isn’t real.

Here are the facts. The preservation age is currently 60, and there are no plans to increase it. Once you reach preservation age, you can access your super if you meet a “condition of release”. That typically means retiring or ceasing employment – though it doesn’t have to be from your main job. Even resigning from a casual job may be enough. And if you’re 60 or older and can’t satisfy a condition of release, you can start a transition-to-retirement (TTR) pension, which allows you to draw up to 10% of your super annually, even while still working. It’s a useful strategy for those wanting to cut back their hours without sacrificing income.

From age 65, you can access your super regardless of your work status

For people on temporary visas, the Departing Australia Superannuation Payment (DASP) scheme allows you to withdraw your super once you’ve left the country permanently. In limited cases, you can access super before preservation age: for example, if you’re permanently incapacitated, terminally ill, suffering severe financial hardship, or facing large medical bills. Each situation has strict eligibility rules and requires approval from the ATO or your super fund.

Super is a long-term investment. But it’s also a tempting target for scammers, because it’s where most Australians keep a large chunk of their retirement wealth. That’s why you need to stay vigilant, question what you see online, and never act on anonymous messages without checking first.

If something sounds extreme or sudden – like moving the preservation age to 70 overnight – don’t panic. Don’t click. Don’t forward it. Just check with a reputable source like your fund, a licensed adviser, or government websites. A moment of doubt can save you a lifetime of trouble.

And finally

Those who jump off a bridge in Paris are in Seine.

A man’s home is his castle, in a manor of speaking.

Dijon vu – the same mustard as before.

Image by stockking on Freepik

Image by stockking on Freepik

Practice safe eating – always use condiments.

Shotgun wedding – A case of wife or death.

A man needs a mistress just to break the monogamy.

A hangover is the wrath of grapes.

Dancing cheek-to-cheek is really a form of floor play.

Does the name Pavlov ring a bell?

Condoms should be used on every conceivable occasion.

Reading while sunbathing makes you well red.

Image by Freepik

Image by Freepik

When two egotists meet, it’s an I for an I.

A bicycle can’t stand on its own because it is two tired.

What’s the definition of a will? (It’s a dead give away.)

Time flies like an arrow. Fruit flies like a banana.

I hope you have enjoyed the latest edition of Noel News.

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker