Noel News 3 Sep

“It’s good to have money and the things that money can buy,

but it’s good, too, to check up once in a while and make sure

that you haven’t lost the things that money can’t buy.”

GEORGE LORIMER

Scammers

Scammers are the big topic this week. I’ve started to receive phone calls on my mobile from strangers telling me that they were simply returning my call. This is puzzling, because these people aren’t criminals, they are simply responding to what they thought was a phone call from me. My question is, how can scammers make a phone call using my number as the originating number? That’s a serious worry.

Then I got an email from one of my golfing friends telling me he wished to send me an email with a question and was that okay. I replied of course. Next thing I got an email along the lines of “I’ve had a bad week financially and I need $400 to tide me over – will pay you back next week.” I know this guy well – and he’s not at all financially challenged. When I phoned him, he told me that many of his mates had gotten the same email. It’s a con.

Furthermore, there have been emails from what appears to be a Gold Coast builder telling me that he had a bill which he owed me for books and I needed to click on the link to download the invoice. It didn’t sound right so I rang him and he told me that he too had been hacked.

I received a text purporting to be from PayPal, telling me that a payment for $1199.10 appeared to be fraudulent, and asking me to ring a number which was highlighted in blue. This was a red flag to me, because there have been warnings recently about texts asking people to click on links that insert malware into your phone.

But I figured it could be important, so to protect myself I dialled the number without clicking on the phone link in the text. A foreign voice answered promptly, “Good morning, PayPal,” and the conversation started.

It didn’t take him long to establish his credentials: he was able to read me the last 10 transactions on my PayPal account, and then told me my correct address and asked me to confirm it. He then said that, to prove his bona fides, PayPal would text me a six-digit authentication number, which I was to read back to him. This duly happened.

Then the conversation turned to credit cards. He claimed a fraudulent transaction had been made on my Virgin credit card. He said the number he had on file started with 4724, and asked me for the other digits on the card, plus the expiry date and the security number on the back.

He then told me he was in contact with Virgin Money, because it was their credit card which had been compromised, but Virgin needed me to authenticate the communication and to do this would text me a six-digit number. This quickly arrived from Virgin, and I read the number to him. This process was repeated several times because, “their computers are slow today.”

A while after the call ended, I got a niggling feeling that something hadn’t been right, and redialled the number he had been phoning me from. The message was, “that number is not connected.”

I became busy with other things, but another red flag was raised when we went out with friends to dinner that night and my Virgin card was declined. I rang Virgin immediately, who identified me using voice recognition – a blessing given the amount of time I’d been on the phone during the day – and they told me there had been six attempted unauthorised transactions on my card during the day. The reason that my caller had been asking me to give him the authenticating numbers from the Virgin texts was to authenticate the fraudulent transactions he was trying to make! Virgin had prevented each one, but of course in stopping them, my credit card got stopped too.

When I reported this whole incident to PayPal, they told me that PayPal never sends texts to anybody – all their communications are by email.

It’s getting scary out there. First of all, how can people make calls that show up as my mobile number, and second, how can people make scam calls to me already knowing my PayPal transactions, my home address and other private information? Be on your guard – the bad guys are getting smarter.

I wrote about this at one of my newspaper columns I got a barrage of emails from readers. What follows is typical.

Brian – You may be interested in an almost exact mirror image of the scam in question using PayPal as the bait, except Westpac have not responded favourably in my case. My situation happened on Wednesday, 18 August, 2021 commencing at approximately 9.30 and involved three amounts $1,878, $2,691 and $3,330. To add salt to the wound, the amounts were cleared today with an additional $80 exchange charge to an account in Kuwait.

I felt uneasy on the day and went immediately to my local Westpac branch and after waiting in a line for 20 minutes, the Teller informed me that it was a scam and there was nothing she could do to stop the payment being processed because I had authorised the payment. She then advised me to immediately talk to the fraud department of Westpac on my own phone. This I did, sitting in the public area at the branch and after waiting until someone was free to speak with me, I was told I had no redress apart from lodging a complaint on the Westpac Bank web site. The complaint was noted and eventually a bank rep will talk with me about the issue. I have been a loyal Westpac customer for over 60 years.

Rob – It has been a stressful week after I was scammed into believing that a screenshot on my computer was from Microsoft Security telling me that my computer had been hacked and that I needed their help do get rid of the hackers in my computer. The punchline was a screenshot that indicated that there were 24 users on my computer, one being Microsoft Security and one being me, with the remaining 22 being scammers that were already accessing my computer data. This was scary, so I was sucked into giving the scammer access to my computer and other personal identification data.

Much loss of sleep and a deep sense of gullibility in being sucked in after warning friends for years to be wary of scams. I have had to notify my bank which closed down all my accounts until my computer was cleared by my computer guru, change all my passwords, and complete a heap of other notifications and reports, and in the meantime days of uncertainty that the issue was safely resolved!

Peter – A bogus email was sent from my email address to my taxation accountant requesting that my tax refund be sent to a different account. The office girl compiled with the request without a phone call to myself for confirmation. Subsequently $8520 was sent. The accountant has requested the bank reverse the transaction and they are in the process of investigating it. I’m told this could take up to 30 days. I’ve made a report to the fraud squad who me the money probably left the country as soon as it was deposited. The ATO tell my they are powerless as the refund was sent to the accountants’ bank and the accountants are saying they were just obeying my instructions.

Bank Share Buybacks

Share buybacks being offered by some of the major banks pose major questions for investors. The big ones are: Why is it happening? What should we do? and What does it mean for the future of the bank shares?

Cast your mind back to early last year, when the COVID-19 crisis was escalating. All the forecasts were of doom and gloom – even the possibility of a major depression. The banks rushed to make provision for the bad debts that were anticipated, and APRA even went to the extent of advising banks to reduce or forego dividends to preserve capital. Bank profits were slashed to make provision for bad debts.

Twelve months later it’s a different world, despite the major lockdowns in some states. The bad debts never eventuated, and banks are now increasing their profits, as well as their dividends, by getting rid of provisions that were never needed. They now find themselves over-capitalised, and are returning that excess capital to shareholders.

So, what does this mean for the future of banks and bank shareholders? If a bank reduces the number of shares it has, and retains its present earnings, investors who retain their shares should see greater earnings and increased dividends per share as time passes. The remaining shareholders will receive a greater share of future dividends than had the buy-back not occurred.

But other issues come into play when deciding whether to sell your shares or keep them. Capital gains tax could be an issue if they are held in your own name or a family trust, but is not an issue if the shares are held by a low income investor or a self-managed super fund in pension mode.

To make it more confusing, NAB and CBA have taken different approaches. NAB are simply going to offer their shares to the market, and anybody who wishes to dispose of their shares, or buy more shares, would do it in the normal way.

The CBA issue is much more complex. The bank is offering to buy a percentage of existing shareholdings at a price which will be based on the bank’s average trading price over the five days leading up to 1 October. Almost certainly it will be at a discount of 14% to the bank’s current price, which was $100 per share at date of writing. The buyback price will comprise two components – a capital component of $21.66 and a fully franked dividend, which will be the difference between $21.66 and the final sale price minus the tender discount.

For example, if the final sale price was $100, the bank would buy them from you at $86 in exchange for a capital payment of $21.66 and a fully franked dividend of $64.34, which would include $27.57 of franking credits. If you are an investor who pays no tax, either because you are on a low income, or because you are in a self-managed superannuation fund in pension mode the franking credits will be refundable to you.

And it gets better; in addition to the above, you will receive a final dividend of $2.00 a share plus all $0.8571 in franking credits. Therefore, your net proceeds should be around $116.43 per share.

Of course, your best strategy will depend on your situation, but it’s hard to see how a retiree could go wrong by joining the tender process. The demand will be massive, which means at best only a small percentage of your CBA shares will be accepted. CBA have announced they will buy the first 100 shares and nobody will be left with fewer than 20 shares, therefore it is reasonable to expect that a parcel of 120 shares would be bought back. And don’t forget, having received an effective $116.43 for each share, you are free to go back into the market and buy more.

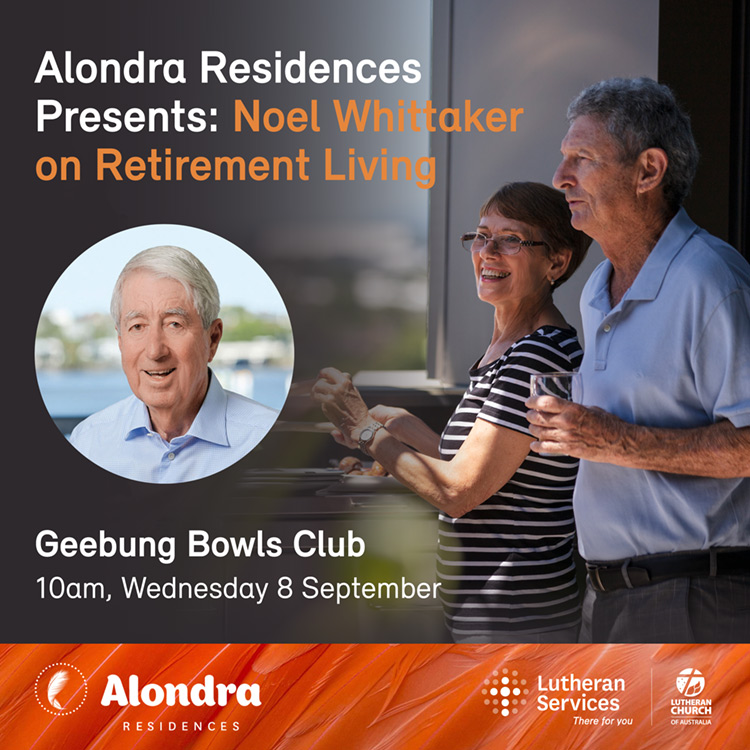

Upcoming Event

Join me next week for a free retirement living seminar where I will be discussing the financial challenges and opportunities facing older people.

Not to be missed, the event includes morning tea and a free copy of my book “Downsizing Made Simple“.

Hurry, places are limited so register today!

Making Money Made Simple

This book has been in circulation for more than 30 years, has sold over 2 million copies, and continues to change the lives of people who read it. Last week I was thrilled to get an email from Ed Vesely an analyst with Motley Fool Australia which is self-explanatory.

In this video which is around 10 minutes long he speaks with Scott Phillips their Chief Investment Officer about Making Money Made Simple and about investing generally. I think you will enjoy it.

“My employer, The Motley Fool Australia, has just started a new YouTube series where each of us discuss a favourite investment book. Naturally, I spoke about yours because it was the first book, and the most important book, I have ever read on investing and personal finance.

It’s just gone up on YouTube and you can watch by clicking on the link here.

https://www.youtube.com/watch?v=ivakY8qmRUc

It was, and is, a great book

Ed Vesely”

Book Updates

Rewritten for New Rules

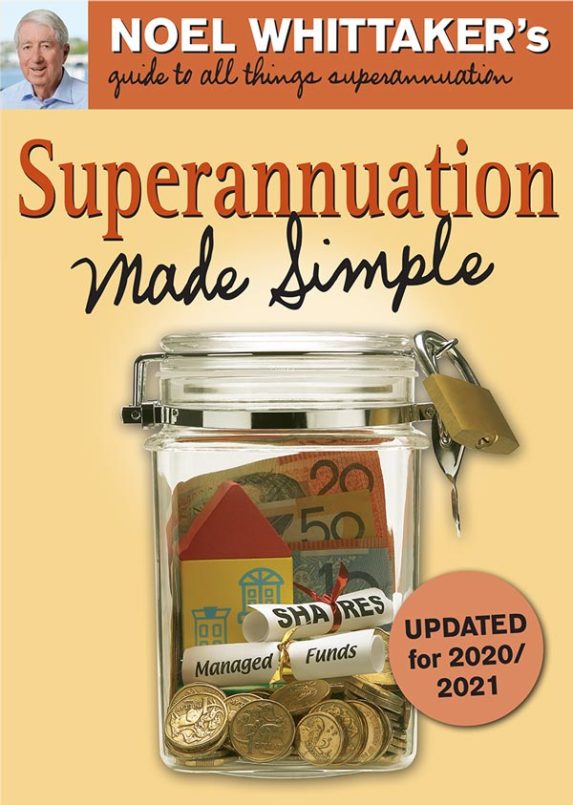

There were some major changes to superannuation that took effect from 1 July 2021 Many of these were due to indexation which increased the amounts that can be contributed, as well as some changes to the age limits.

There are also major changes that should take effect from 1 July next year.

My book Superannuation Make Simple has been totally rewritten to take account of these new rules.

It just happened that both Retirement Made Simple and Making Money Made Simple needed reprints too which gave me the opportunity to incorporate the changes to superannuation in these books as well. All these books are available from my website.

Just a few left

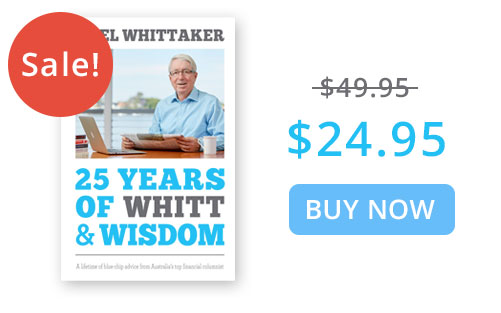

A few months ago I mentioned two books which will be going out of print and which I’m keen to clear. They have nearly all sold but I’ve got just a few left. Do you know I’m slashing the price to $24.95 for each book.

The first is 25 Years of Whitt & Wisdom – a hard cover 450 page very attractive book in high-quality paper. It’s not just a wonderful history of the 25 years when the Australian financial services industry was coming-of-age, it also contains a wealth of timeless value. It is still one of my favourite books and a great book to browse through.

The other is the international bestselling book written by my son James Whittaker that accompanied the film Think and Grow Rich: The Legacy, which we launched in Los Angeles in 2018. This book is a timeless classic. Not only does it introduce the original Think and Grow Rich principles in a modern context, it also includes firsthand accounts of how some of the most successful leaders on the planet today used those principles to achieve massive success. If you want a blueprint to growth, and the inspiration to make it happen, I can’t recommend it highly enough.

We have a limited supply of 250 copies left, which we’re reducing to $24.95.

As a special bonus to my loyal readers I’m going to let you have a copy of the updated edition of Superannuation Made Simple to anybody for just $5 who buys one of these two books. The retail price of the Superannuation book is $24.95 – the bundles of two are just $29.95. That’s a huge saving.

And finally…

Some thought provoking ideas for those of us whose day is filled with the mundane………

What’s the speed of dark?

What’s the speed of dark?

How come abbreviated is such a long word?

Why are they called apartments, when they’re all stuck together?

If you got into a taxi and the driver started driving backward, would the taxi driver end up owing you money?

Why is a carrot more orange than an orange?

When two airplanes almost collide why do they call it a near miss and not a near hit?

Why are there 5 syllables in the word “monosyllabic”?

Why do scientists call it research when looking for something new?

If “con” is the opposite of “pro,” then what is the opposite of progress?

What do little birdies see when they get knocked unconscious?

If all those psychics know the winning lottery numbers, why are they all still working?

Why do we put cargo on a ship, and shipment in a truck?

Can vegetarians eat animal crackers?

If man evolved from apes why do we still have apes?

I went to a bookstore and asked the saleswoman where the Self Help section was, she said if she told me it would defeat the purpose.

Should crematoriums give discounts for burn victims?

If a mute kid swears does his mother wash his hands with soap?

And whose cruel idea was it to put an “S” in the word “Lisp”?

If a man stands in the middle of the forest speaking and there is no woman around to hear him….Is he still wrong?

If someone with multiple personalities threatens suicide….is it considered a hostage situation?

Is there another word for synonym?

Isn’t it scary that doctors call what they do “practice”?

Where do forest rangers go to get away from it all?

What should you do if you see an endangered animal eating an endangered plant?

If a parsley farmer is sued do they garnish his wages?

Would a wingless fly be called a walk?

Is a shell less turtle homeless or just naked?

Is it true that cannibals won’t eat clowns because they taste funny?

Why do they put Braille on the drive through bank machines?

Do they use sterilized needles for lethal injections?

Why did kamikaze pilots wear helmets?

What was the best thing BEFORE sliced bread?

I hope you have enjoyed the latest edition of Noel News.

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get much more regular communications from me if you follow me on twitter – @NoelWhittaker.

Noel Whittaker