CUSTOMER SERVICE

Technology has revolutionised payment for goods and services. Forty years ago, Bankcard was introduced to great fanfare, and we were bowled over by the convenience it offered.

Today we have contactless payments such as PayWave offered by Visa, and PayPass offered by MasterCard, and even hints from Apple that we will soon be able to pay with our mobile phone. And consumers are taking to it in droves – today over 50% of transactions are tap and go.

I love the new technology but unfortunately, there are some retailers who are still in the dark ages – usually small business operators. It’s a great pity, because small business is the lifeblood of Australia, and the one place where it’s possible to get personal service. Everybody is tired of faceless institutions who keep you on hold for ten minutes, while you listen to recordings of how much they value your business, and how the conversation will be monitored for quality control to ensure the mediocre service they are giving is perpetuated.

Never has there been a more appropriate time for small business to step up to the plate and treat their customers as people to be cared for – not things to be ignored.

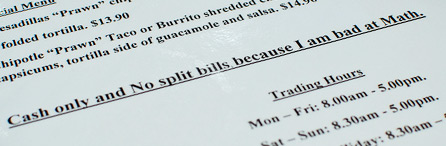

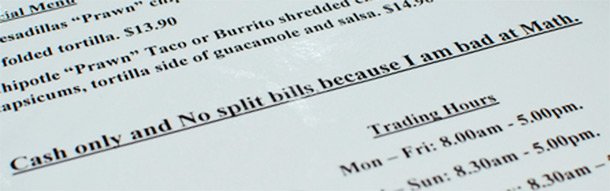

Sadly, there are still many small business owners who are more intent on erecting negative signs than offering service. Think about the coffee shop I went to recently – they make good coffee, and would be justified in having a large sign at the front door that says ‘Come Inside For A Great Coffee’. No way – their front door sign says ‘No Split Bills’. Imagine the message that gives.

My pet hate is establishments that display a sign ‘No EFTPOS Accepted Under $10’. There may have been some justification for this prior to tap and go because EFTPOS transactions do have a flat cost, as well as a percentage cost. It would be unrealistic for the retailer to pay a fee of say, 20 cents, on a transaction of a couple of dollars in addition to the normal percentage charged by the bank.

But, there are no flat fees on tap and go transactions, so there is no justification for the sign. I have questioned retailers at length as to why they want to set a minimum for tap and go payments. Invariably they um and ah, and mumble something about high bank charges – when asked to specify what the charges are, they confess they don’t have a clue.

Apparently, objections to tap and go fall into two categories. The first is that many retailers believe there is no cost to handle a cash transaction, whereas there is a cost to handle an electronic transaction. It has never dawned on them that there is a cost in receiving the money from a cash transaction, calculating the change, balancing the till, preparing the bank deposit, and then standing in line at the bank to deposit the money.

Or else they simply want to put cash in their own pocket and bypass the taxman. As one savvy retailer pointed out to me “if I can skim the till – my staff can skim the till”.

In any event, the ambition of most people with their own business is to build it up and sell it. The sale price will invariably be calculated on the turnover and profits of the business, which are inexorably linked to the amount of money the business receives. Skimming the till might put a few dollars in your pocket in the short term, but means a much lower price for your business in the long term.

Service is the secret of a successful small business – tap and go is an easy way to improve it.